That is log of the complementary cumulative Normal distribution function. The sum of logs complicates things. But we can see that this is non-convex even if there is no sum (i.e., sum has one term).

Exponentiate (6) and then take log again, resulting in log_normcdf(u) <= log(1-exp(alpha)) . This is going in the wrong direction to be convex, because log_normcdf is concave.

Thanks you for your kind help.

Note that I’ve miss-typed RHS on (6). alpha should be converted to log(alpha) as well as left side hand terms.

Having log on the alpha doesn’t change the non-convexity assessment.

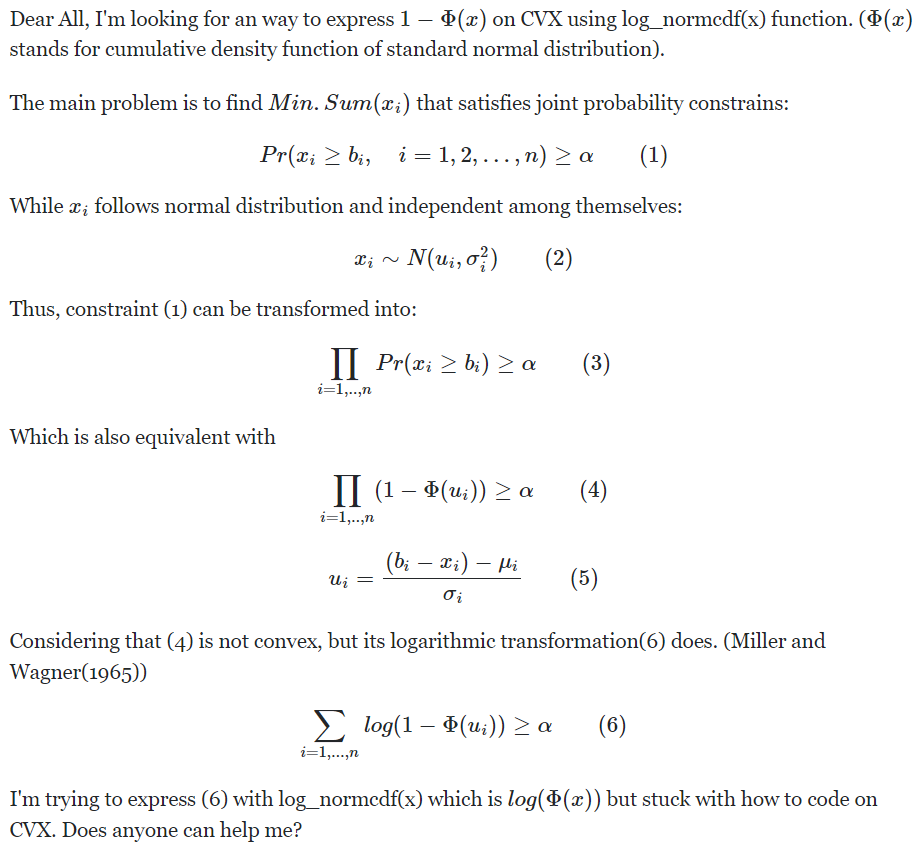

Dear Mark,

I’ve changed complementary cumulative Normal distribution term in (6) with \Phi(-u_i)

and got reasonable outcomes using CVX. (verified it by feeding various parameters into Normal distribution and watched that they’ve satisfied \alpha constraint)

This may be one of the promising breakthroughs I guess.

Yes, I should have thought of that. Complementary symmetry is your friend.