Hi, I tried to programming a log-optimal optimization with matlab by using CVX

The code is refer to Exercise 4.60: Log-optimal investment strategy in Boyd & Vandenberghe “Convex Optimization”, and I change the input of it

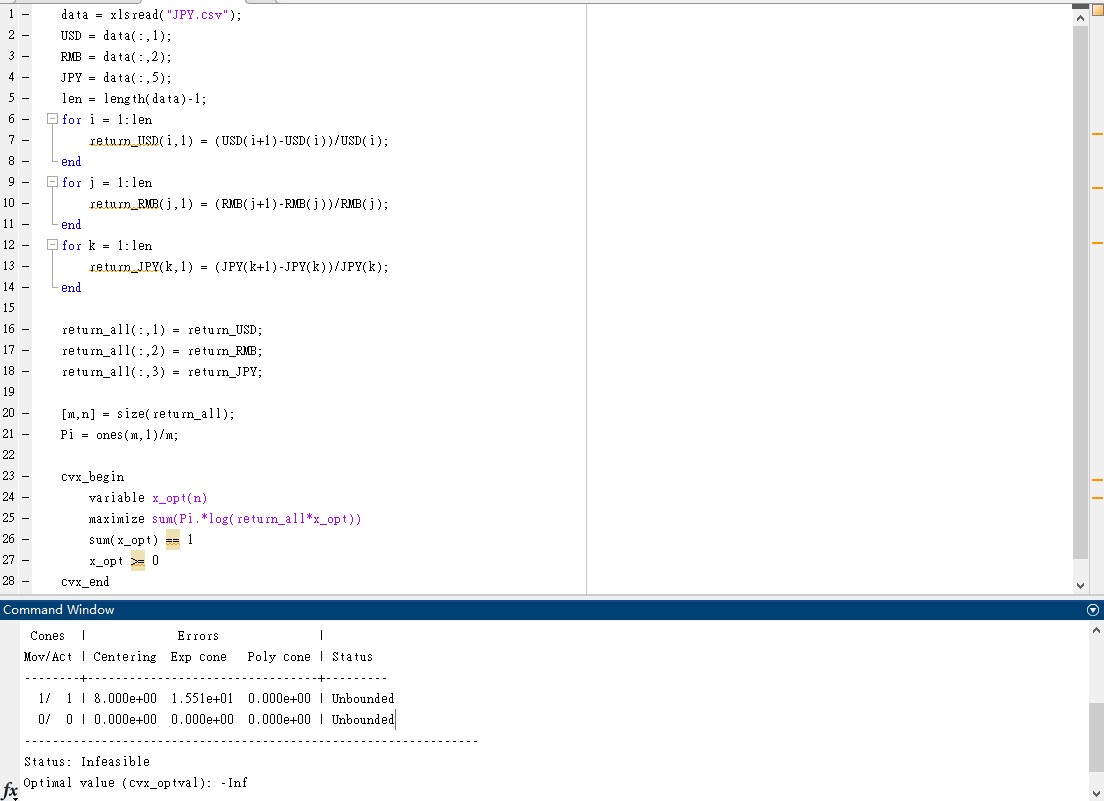

Here is the code

It may be that your input data is badly scaled numerically. Change units if necessary so that all non-zero input data is within a small number of orders of magnitude of 1. Maybe some of the numbers in data are` tiny, and should be set to be exactly zero, or their differences are tiny, and those differences should be set to exactly zero? Perhaps the objective is coupling into the constraint to make is appear numerically infeasible, even though the problem is clearly feasible.