Hello,

Example:

cvx_begin

variable Sigma2(n,n) symmetric

maximize ( w'*Sigma2*w )

subject to

Sigma2 == semidefinite(n); % Sigma2 is positive semidefinite

Sigma2(1,1) == 1

Sigma2(1,2) >= 0

Sigma2(1,3) >= 0

Sigma2(2,1) >= 0

Sigma2(2,2) == 1

Sigma2(2,3) <= 0

Sigma2(2,4) <= 0

Sigma2(3,1) >= 0

Sigma2(3,2) <= 0

Sigma2(3,3) == 1

Sigma2(3,4) >= 0

Sigma2(4,2) <= 0

Sigma2(4,3) >= 0

Sigma2(4,4) == 1

cvx_end

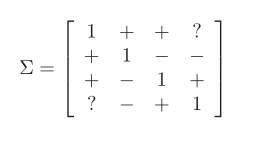

Can express these constraints with two matrices L and U instead of by elements? These are the constraints:

I tried:

U =

1 Inf Inf Inf

Inf 1 0 0

Inf 0 1 Inf

Inf 0 Inf 1

>> L

L =

1 0 0 -Inf

0 1 -Inf -Inf

0 -Inf 1 0

-Inf -Inf 0 1

But this constraint is not convex.

Error using cvxprob/newcnstr (line 192)

Disciplined convex programming error:

Invalid constraint: {real affine} >= {invalid}Error in >= (line 21)

b = newcnstr( evalin( ‘caller’, ‘cvx_problem’, ‘’ ), x, y, ‘>=’ );Error in cvx_proba2 (line 6)

Sigma2 >= L;

cvx_begin

variable Sigma2(n,n) symmetric

maximize ( w'*Sigma2*w )

subject to

Sigma2 == semidefinite(n); % Sigma2 is positive semidefinite

Sigma2 >= L

Sigma2 <= U

cvx_end

Thank you.